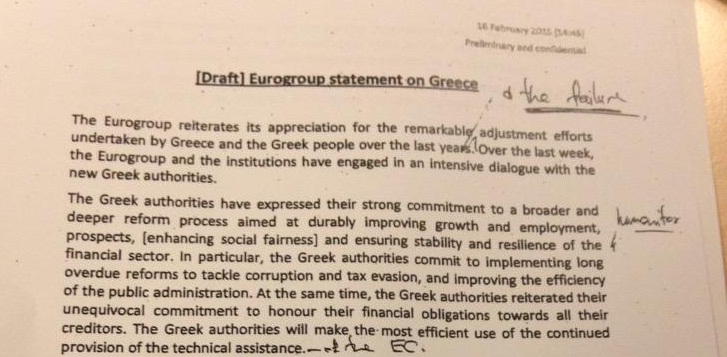

24 February 2015 Greece continues to be financed with the help of the European Union. Eurozone Ministers of Economy and Finance have approved the new package of economic measures presented to Brussels by Athens. This then paves the way to extend Greece’s bail-out.

The green light was confirmed by Vice President for the Euro and Social Dialogue, the Latvian Valdis Dombrovskis, and the Slovak Minister of Finance, Peter Kazimir, through their respective accounts on Twitter. In a brief statement the Eurogroup, chaired by Dutchman Jeroen Dijsselbloem, called on “the Greek authorities to further develop and broaden the list of reform measures, based on the current arrangement, in close coordination with the institutions”. Based on the tentative agreement reached between Greece and its official creditors last 20 February, approval of the list was a condition for extending the availability of bail-out funds for another four months. The current programme, which has buoyed up the most indebted country in Europe, was scheduled to conclude later this month.

Course reversal over the national minimum wage and nationalizations

Alexis Tsipras’ list of government commitments is not very explicit, in any case, and does not translate into concrete figures. Currently it fails to meet two of the election promises which the leader of the radical left party, Syriza, came to power with: the increase in the national minimum wage and the (re)nationalization of companies. The list still includes a promise to introduce a guaranteed basic income scheme to discourage early retirement. According to the Athens government, one has to ask for a lot of things to get even 5% of them.

Greece “will not reverse privatizations already completed or which have already gone through auction”. Privatizations that have not yet been put in place will be reviewed, to maximize the long-term benefit for the State and generate revenue. The Troika, a body that has now become the “institutions”, will have to smooth out their differences with Athens over this point. So far, the Commission, the International Monetary Fund (IMF) and the European Central Bank (ECB) have also given their approval.

The spokesman for the European Commission, Margaritis Schinas, said that the proposals are “sufficiently complete” and are a “good start”. The same expression was used by Mario Draghi in a statement, however the ECB president added several ‘buts’. According to Draghi, what counts is the current memorandum. The IMF has also expressed some doubts. Its managing director, Christine Lagarde, in a letter to Dijsselbloem, said that the list of Greek reforms has no guarantees of implementation. “We believe these commitments to be critical to the ability of Greece to meet the basic objectives of its aid programme,” said Lagarde.

Misgivings over the reform package

Reservations both on the part of the IMF and the ECB could do a favour to Tsipras. The Greek Prime Minister, after “betraying” his electorate and the grass roots of his party, will have got something back from these two, theoretically less politicized, institutions. What is certain is that for the time being Greece has already won more time and money. What is not certain, however, is the political cost that this will have for the Greek government. Tsipras faces a tough battle amongst the ranks of his party. Holding Syriza together will not be easy for the Prime Minister, while he negotiates with his most sceptical counterparts in the Eurozone, as is Germany.

The IMF and the European Bank are also wary of compliance with the package of measures proposed by Greece because they want more details, e.g. on taxation. Athens is committed to a reform of VAT to combat tax evasion – huge in sectors such as cigarettes or fuel. To combat fraud the Greek government will create an independent tax council; modernize public finance; and increase the number of inspections.

Combating corruption is “a national priority” for the government of Tsipras, which promises greater tax collection without specifying any figures. The list of reforms includes reducing the number of ministries from 16 to 10 and tightening up legislation on party funding. The pay scale for civil servants is also to be reformed, in line with productivity.

Banks benefit the most

The banks are a different matter. Greek credit institutions are to use European funds to stabilize the financial sector and the default rate will be regulated on the basis of the level of bank capitalization. And finally, a curious and troubling measure: Athens undertakes, from now on, to ensure the reliability of its statistics.

While the green light from the Eurogroup is no immediate support for the banks, it does represent a lifeline for Greece’s financial system, which has seen spectacular capital flight: more than €20bn has gone from the country’s bank deposits since Syriza came to power last month. The ECB will wait for its monetary policy meeting in March before re-establishing its credit line to Greek banks.

The new package for Greece is subject to the formal consent of national parliaments. Germany, Finland and the Netherlands are the countries that are the most wary of this agreement but it does not seem likely that they will stand in the way, once their governments approve the extension of aid to Greece.

The Athens Stock Market has celebrated the agreement in style. Its overall index rose 9.8% to touch its highest level since early December last year. The banks have been the big winners. National Bank of Greece shares have climbed by 14%, 13% for Alpha Bank and 11% for Piraeus Bank. So far this month, the sector index is up by 50%, a 70% rise from the lows it reached the day after the 25 January elections.

From the ECB, Danièle Nouy, who is in charge of bank supervision, has said that Greek financial institutions are solvent and able to cope with the current difficulties in the form of capital flight. Even so, bank stock has lost, on average, 85% since early 2012.